A 1031 exchange, also known as a like-kind exchange, is a provision in the United States Internal Revenue Code (Section 1031) that allows investors to defer capital gains taxes on the sale of certain types of business or investment properties, as long as they reinvest the proceeds into another qualifying property. The main purpose of a 1031 exchange is to encourage investment and facilitate the free flow of capital within the real estate market.

There are several factors to consider when conducting a 1031 exchange:

1. Qualifying Properties

To qualify for a 1031 exchange, both the property being sold (the relinquished property) and the property being acquired (the replacement property) must be held for investment, business, or productive use. Personal residences do not qualify for a 1031 exchange. However, a few specific types of properties, such as vacation rentals or properties held primarily for resale, may also not qualify.

2. Timeframes

There are strict timelines associated with a 1031 exchange that must be adhered to. After selling the relinquished property, the investor has 45 days to identify potential replacement properties in writing to a qualified intermediary (QI). The replacement properties must be clearly identified within this 45-day window. Then, the investor has a total of 180 days from the sale of the relinquished property to complete the acquisition of the replacement property.

1031 Exchange Timeline

Property exchangers must follow a specific timeline to take advantage of the benefits of a 1031 transaction. The entire 1031 transaction can take no longer than 180 days.

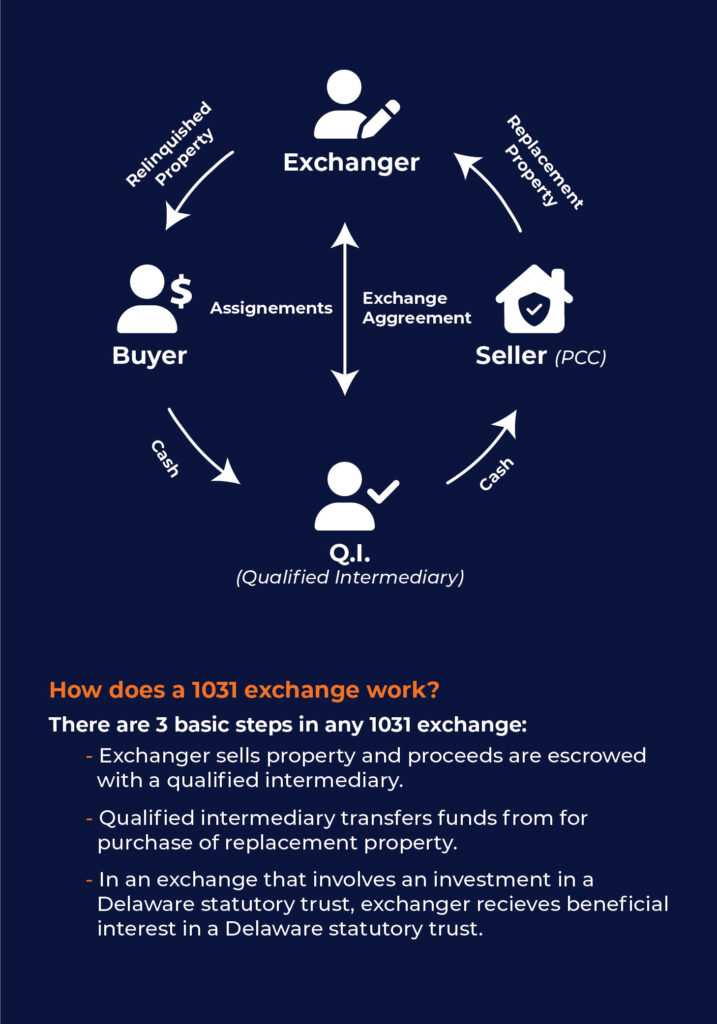

3. Qualified Intermediary (QI)

To ensure the exchange is valid, a qualified intermediary must be involved. The QI is an independent third party who facilitates the exchange process, holding the proceeds from the sale of the relinquished property in escrow until they are used to purchase the replacement property. It is essential to avoid direct receipt of the sale proceeds by the taxpayer to maintain the tax-deferred status.

4. Equal or Greater Value and Equity

To fully defer taxes, the value of the replacement property must be equal to or greater than the relinquished property, and all the net proceeds from the sale of the relinquished property must be reinvested into the replacement property. If the replacement property has a lower value or the investor takes out cash, the difference is considered “boot” and may be subject to capital gains tax.

5. Like-Kind Requirement

Contrary to what the term “like-kind” might suggest, the properties involved in the exchange do not need to be identical. The IRS has a relatively broad definition of “like-kind” for real estate, which means that most types of investment or business properties can be exchanged for others, as long as they meet the investment or business-use requirements.

By utilizing a 1031 exchange, investors can continue to grow their real estate investments without incurring immediate capital gains taxes, thereby providing an opportunity for increased wealth accumulation and portfolio diversification. It is crucial to consult with tax and legal professionals experienced in 1031 exchanges to ensure compliance with all IRS regulations and requirements.